Well, it's true there are many implementations avalable such as the one in the book Financial Numerical Recipes. However, the problem is that we have to compute literally hundreds of thousands IRRs, and I couldn't find an algorithm, which would always find IRR. I think that most of them, like Excel, use some variation of Newton-Raphson algorithm. For example, in our case sometimes up to 1% of IRRs were not found or "wrong" IRRs were returned.

By "wrong" IRR, I mean IRR less than -1, such as -1.6, i.e. -160% monthly interest rate. The problem is that there's another IRR for the same cashflow, which is a "good" one, it was 0.25, i.e. 25% monthly. Such cases were labeled wrongly "miltiple IRR" cases. However, we'll see later on that the problem is not the multiplicity of IRRs, but the fact that our routines find IRRs on the left side of IRR = -1. These IRRs produce amortization schedules which are unacceptable for certain reasons.

I came up with an algorithm, which almost always finds good IRR, but I'll write about it later. Here, I'm going to share with you my little math analysis of typical MBS cashflows.

The typical MBS cashflow is the one with initial payment (outflow) and subsequent cash inflows. So, if Cm is the cashflow amount of month 'm', then C1 < 0, and all other Cm > 0. For example, C1 = -100$ - initial payment, then C2 = 10$ and C3 = 110 cash inflows.

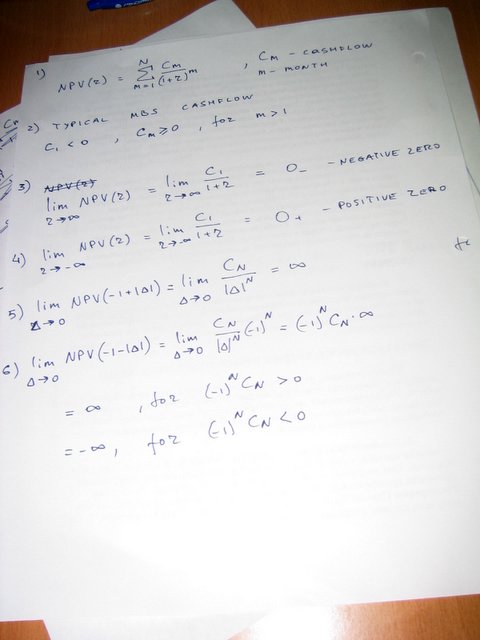

Net present value (NPV) of the cashflow is a sum of terms: Cm/(1+r)^m , where m - is month number, Cm - cashflow amount, r - interest rate. So, in our case it's C1/(1+r)+C2/(1+r)^2+C3/(1+r)^3. IRR is defines as interest rate r, such that NPV(r)=0. In our example it's 0.1, or 10% monthly, see:

| Month | Cashflow | IRR | NPV(IRR) | |

| 1 | -100 | 0.1 | -0.000000000000028 | |

| 2 | 10 | |||

| 3 | 110 |

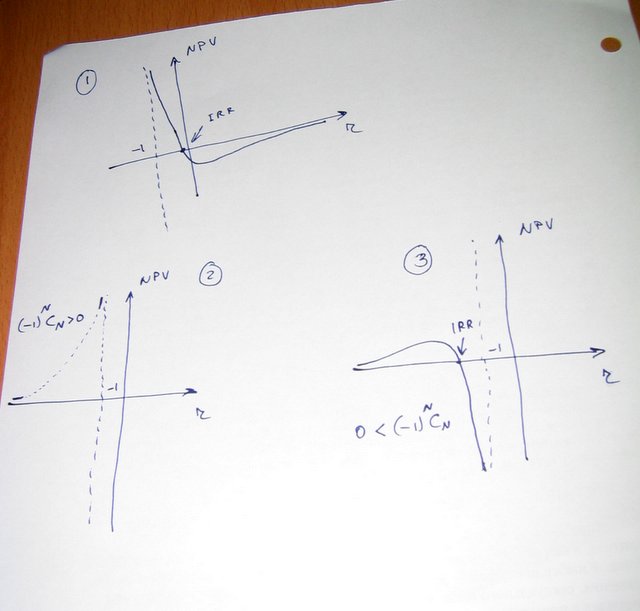

A bfrief analysis of the NPV function, given the assumptions of "typical MBS cashflows", brings the following results:

- As it's shows on figure 1, there's at least one real IRR, which is greater than -1, because NPV(-1) is positive and NPV(infinity) is negative on the right side of -1 rate.

- If Cn*(-1)^n > 0, where n - last month with non-zero cashflow amount, then NPV(-1) is positive and NPV(infinity) is positive on the left side of -1 rate. This means that we can't say if there's real IRR on left side. See figure 2.

- If Cn*(-1)^n < 0, where n - last month with non-zero cashflow amount, then NPV(-1) is negative and NPV(infinity) is positive on the left side of -1 rate. This means that there's at least one IRR on left side. See figure 3.

Since we have Cn positive, then cases 2 and 3 degenerate to a condition (-1)^n.

You can look at my notes on how I came to above conclusions in the

next picture. Basic idea is too look at behaviour of NPV near rate values of -1 and negative and positive infinities. Near rate equal to -1, the latest cashflow amounts (which is positive) is most significant, because 1/(1+r)^n is the most significant term.

next picture. Basic idea is too look at behaviour of NPV near rate values of -1 and negative and positive infinities. Near rate equal to -1, the latest cashflow amounts (which is positive) is most significant, because 1/(1+r)^n is the most significant term. On the other hand, near infinities the most significant term is C1 (initial payment), because 1/(1+r) is the most significant.

Conclusion for "typical MBS cashflows":

- there's always real IRR between -1 and positive infinity.

- if the month number of the last non-zero cashflow amount is odd, then there's at least one real IRR between -1 and negative infinity.

- quite often there are more than one real IRRs.

Enjoy!

2 comments:

Hi,

You wrote: "I came up with an algorithm, which almost always finds good IRR, but I'll write about it later."

I'd be very interested in learning more about your findings. I'm working on IRR calculations for Private Equity investments, and usually get meaningful IRR's using the plain-vanilla Newton-Rhapson method, but occasionally the initial guess is too far off (I use either Modified Dietz, if meaningful, or Modified IRR using a reinvestment assumption = the minimum possible return).

I'm debating on whether I need to fine-tune my initial guess, use a more powerful root-finding algorithm, or both to deal with these corner cases. I notice that Excel's XIRR and Solver functions can solve most of these using my initial guess, or even a much weaker guess, leading me to believe that they're using a more powerful quasi-Newton method.

Hi

I wrote a function which [almost] always finds IRRs but my client decided to patent it, so I can't disclose it.

However, there are other ways to do it, depending on your circumstances. For example, writing an Excel utility, which is supposed to be run by your analyst is very different from the server-side library to be run on 1 million cashflows without user intervention.

If you dont need the fastest algorithm, then I recommend to look at Matlab's roots function. It's based on the fact that you can reduce IRR finding to eigen values problem. No guess is needed, works like a charm for me. Let me know if you have issues

Post a Comment